Want to cut unnecessary costs, optimise the most profitable parts of the business, and increase your overall return on investment?

Talk to us about how we can work with you to support your ongoing business profitability.

Turning a profit will be high on your list of goals as a business owner. And if you want to generate the best margins, that means keeping an eye on the money that’s going out of the business, as well as what’s coming in.

So, how can your accountant help with this?

The days where your accountant just did the bookkeeping, compiled your accounts and filed your tax return are well and truly over. Modern accounting firms are far more interested in helping you with your financial performance, your business strategy and offering flexible value-add services that put you in better control of your finances.

If you partner with the right accountant, we can actually save you money – in both the short, medium and long-term. And that’s good news for the growth of your business.

Key ways your accountant can enhance your financial health

The less expenditure you have as a company, the bigger your profit margin. It sounds incredibly simple, doesn’t it? – The smaller your costs, the larger your profit. But if you’re not fully in control of your financial management, it’s very difficult to know WHERE you’re spending money, and WHY you’re not achieving your profit targets.

This is where working with a finance professional adds a huge amount of value. Your accountant helps put you back in the driving seat of your finances – and that’s never been more needed than in the current economic climate.

So, what specific things can your accountant do and what will the impact be on the future of your business?

Tax advice and planning – tax costs can be one of your biggest outgoings as a business, so we’ll focus on getting your tax planning under control, applying for all the relevant tax incentives and ensuring you minimise the taxes on your profits. By paying only what you’re legally required to pay – and making use of any reliefs – we can significantly cut your tax spend in the business.

Cashflow management and advice – ‘Cash is King’ may be a cliche, but it’s true. Unless you can balance the cash inflows and outflows from your business, you’ll never have the liquid cash to pay your bills, cover your payroll costs or cover your operational expenses. We’ll show you where money is going out, and coming in, so you achieve the ideal positive cashflow position.

Cost control and spend management – to improve your cashflow, you need to reduce your cash outflows. An important way to do this is to focus on cost control and spend management, reducing your expenditure, removing unnecessary costs and negotiating better deals with your suppliers. The more you cut costs back, the better your cashflow will be and the easier it will be to thrive, grow and become more profitable.

Forecasting and financial modelling – when we understand the key financial drivers in your business, we can build you a full financial model. This allows us to change the variables, run different scenarios and forecast the various future paths of your business. Being able to project these numbers forward gives you a clearer view of the path ahead – and that’s invaluable in the challenging economic times that we all face at present.

Better management reporting and information – your decision-making stands or falls on the information you have available to you. We provide detailed management accounts, breakdowns of key metrics and forecasts of your cashflow, spending, aged debt and revenue – all of which helps you to save money, make sound decisions and keep the revenues flowing into your business.

Talk to us about cutting costs and boosting profits

Rather than running your business on a wing and prayer, by working with an accountant you get a clear picture on your business financials. We’ll help you cut unnecessary costs, optimise the most profitable parts of the business and increase your overall return on investment.

Let’s talk about how we can work together to support your ongoing business profitability.

The ATO has finalised its compliance approach in relation to the integrity measure in s 207-159 of ITAA 1997, which operates to make certain distributions funded by capital raising unfrankable.

The ATO has finalised the Practical Compliance Guideline PCG 2025/3, which outlines the types of arrangements that may be at a risk of non-compliance with the s 207-159 of the Income Tax Assessment Act 1997 (ITAA 1997).

The new guideline should be read along with the Taxpayer Alert TA 2015/2, issued by the ATO in May 2015, addressing their concerns regarding arrangements where private companies raise funds (often through debt or equity) to make distributions to shareholders, particularly where the distributions are debited to the share capital account rather than retained earnings.

Types of distributions under scrutiny

In effect from 28 November 2023, s 207-159 of the ITAA 1997 applies to deem certain distributions funded by capital raising activities unfrankable if they fail to meet a prescribed criterion.

The legislative restrictions may apply if the relevant distribution does not meet the following requirements as outlined in the PCG 2025/3:

Consistency with established practice — the entity does not have an established practice of making distributions of that kind, or, if it does have an established practice, the relevant distribution does not align with that practice.

Equity interests issued — there must be an issuance of equity interests by the company or related entities around the time of the relevant distribution.

Principal effect and purpose — the equity interests were issued for a purpose (other than incidental) to directly or indirectly fund a substantial part of the relevant distribution.

No regulatory requirement — the equity issuance is not a direct response to regulatory requirements from APRA or ASIC.

Next steps

This finalised guidance is ATO’s reminder that arrangements lacking genuine commercial purpose and designed primarily for tax advantage may be subject to anti-avoidance rules and recharacterisation.

There may be many implications for arrangements where s 207-159 applies to a dividend distribution.

Implications for shareholders include:

Shareholders receiving an unfrankable distribution do not receive a tax offset for the franking credits, as there are none attached to the distribution. This means they cannot reduce their tax liability using franking credits.

Without franking credits, shareholders may face a higher effective tax rate on the distribution, as they must pay tax on the full amount of the distribution without any offset for tax already paid by the company.

Non-resident shareholders may be subject to withholding tax on unfrankable distributions, as these distributions do not benefit from the imputation system that typically reduces or eliminates withholding tax.

Implications for the distributing entity include:

No franking debits get recorded for an unfrankable distribution.

The ATO will closely examine distributions that appear artificial or contrived, particularly that do not align with an entity’s historical distribution practices, non-compliance with the guidelines may lead to penalties and adjustments in tax obligations.

If you’re incurring expenses as part of your job or self-employment, you can claim some of these expenses back and lower your overall income tax bill.

As an individual taxpayer, you know it’s mandatory to submit your annual tax return to the Australian Taxation Office (ATO) at the end of each financial year (ending each June).

Did you know that you claim expenses against some of your work and personal expenses?

Let’s look at what expenses you can claim and the process for reducing your taxable income.

What’s your taxable income?

You only pay tax on what’s known as your ‘taxable income’. By making an eligible claim for expenses, you can reduce the total of this taxable income. In short, this means you will pay less in tax – with the tax deductible items deducted from your total taxable income.

Work-related expenses you can claim

If you’re incurring expenses as part of your job or self-employment, you can claim some of these expenses back and lower your overall income tax bill.

To claim a deduction for a work-related expense:

You must spend the money yourself and not get a reimbursement

The expense must directly relate to earning your income

You must have a record to prove it (usually a receipt) Costs that you may be able to claim against include:

Cars, transport and travel expenses

Tools, computers and items you use for work

Clothes and items you wear for work

Working from home expenses

Education, training and seminar expenses

Memberships, accreditations, fees and commissions

Some meals while working overtime

Medical and health expenses Not all tax deductible expenses relate to your employment. There are other areas where you may be able to reduce your taxable income.

These include:

Gifts and donations

Expenses related to earning income from investments

Personal super contributions

Income protection insurance

The cost of managing your tax affairs. How to make a claim for expenses

Keeping records is a vital part of making a claim for expenses. The ATO will need to see receipts and records that show you incurred the expense.

You can use the myDeductions tool in the ATO app to help keep track of your work-related expenses (such as vehicle trips) and general expenses (such as gifts and donations).

These records can be uploaded when you lodge your return online with myTax, or you can share them with us, as your registered tax agent and accountant. Talk to us about about making a claim for expenses Claiming the expenses you’re due can make a big difference to your tax bill.

Talk to our team about setting up the right record-keeping processes and claiming the tax deductible expenses that you’re eligible for, both in and out of work.

A business credit card could be an excellent way to start building your company’s credit profile. We’ve listed five benefits of applying for a business credit card.

At the early stages of your start-up journey, access to credit can be a lifesaver.

Cashflow is tight, customer revenue can fluctuate wildly and large-scale bank loans and external funding may be in short supply. In this situation it might seem counterproductive to apply for a business credit card – a move that adds to your debt level.

But, in fact, applying for a company credit card and using that credit facility responsibly can have a hugely positive effect on your ability to fund your growth and access lines of credit. Let’s explore five ways that a business credit card can improve your funding

Builds up your business credit profile

When you use a business credit card responsibly, and pay off the repayments each month, this starts to build up a credit history for the company. This credit profile is directly linked to your business and is separate from your own personal credit.

Having this credit history (and the associated business credit score) is crucial when applying for business loans and accessing future, large credit lines.

Establishes you as a responsible borrower

Paying your credit card bill on time each month demonstrates your financial discipline and an ability to manage debt in a responsible way.

When applying for loans, bank overdrafts and trade credit, lenders want to know that you’re a low-risk business to lend to. Responsible payment behaviour acts as an indicator of trustworthiness for future borrowing and will increase your chances of successful funding.

Provides a flexible line of credit

Having a business credit card makes it easier to cover your expenses and overheads.

A credit card gives you flexible, accessible funds for your day-to-day operational needs. It’s also an excellent way to cover any unexpected expenses or cashflow gaps. Managing this line of credit also prepares you for larger, more formal, credit facilities.

By not maxing out the available credit on your credit card, and keeping utilisation low, you can show that your business manages debt in a sensible way. This marks you out as a low-risk borrower – a key factor in accessing further credit, business finance and investment..

Acts as a gateway to more favourable terms

By being responsible with your credit use, you set the foundations for a business credit profile.

A solid track record with a business credit card may lead to pre-approved offers for larger credit lines, better interest rates and more flexible terms from banks. This is incredibly helpful as you scale the business and need additional funding to drive your growth journey. Talk to us about applying for credit and business finance

If your startup is in need of an increased cash runway and improved access to credit, applying for a business credit card is an excellent way to improve your financial flexibility.

Come and talk to the team about ways to embrace this kind of credit.

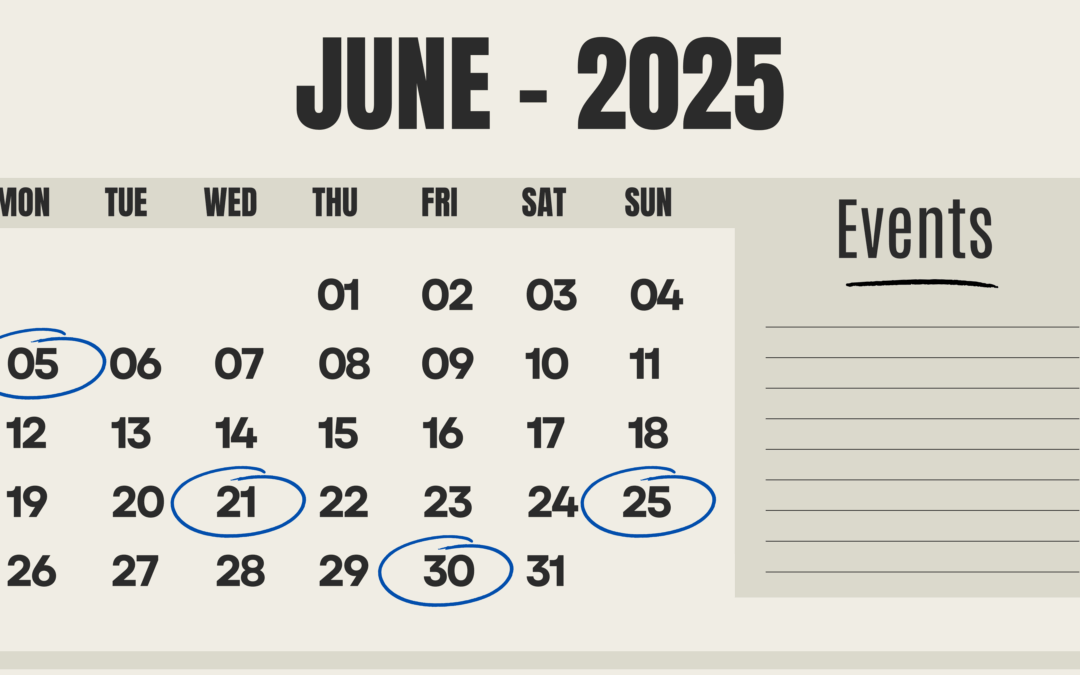

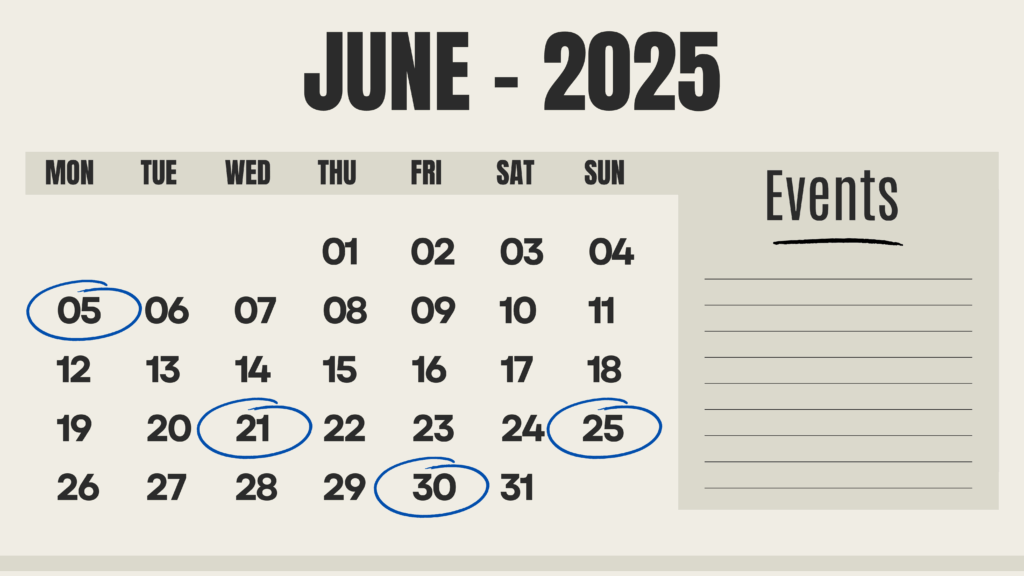

With the end of the current tax year upon us, please do not forget about your final tax obligations for 2025. Here is a list of key tax dates for June 2025.

The end of the current financial year is upon us. For most of you, this means preparation to start finalising your general ledger accounts for the upcoming end of year compliance.

In order for you to be across all upcoming due dates and deadlines, please find a list of the key compliance dates below for June 2025. Make sure these lodgments are up to date to avoid any interest or penalties.

KEY TAX DATES – JUNE 2025

5 June 2025 – Income tax – Due date for lodgment of tax returns of all entities 5 June concession. Note: Entities eligible for the 5 June 2025 concessional due date can lodge by 8 June 2025, as long as any liability due is paid by this date. You do not need to apply for a deferral.

21 June 2025 – GST – Monthly Activity Statement and payment for May 2025

21 June 2025 – PAYG withheld and PAYG instalment – Monthly Activity Statement and payment for May 2025

25 June 2025 – FBT – Lodge 2025 FBT annual return for tax agents if lodging electronically, if you are lodging with us

30 June 2025 – Superannuation guarantee – Super guarantee contributions must be paid by this date to qualify for a tax deduction in the 2024–25 financial year.

We’re here to help if you’re facing operational issues, tackling people challenges, or have health and safety questions, give us a call, email or text us.

The way to calculate a working from home deduction using fixed cost method for additional running expenses has been adjusted from 1 July 2024, with the ATO issuing a new hourly fixed rate.

The Australian Taxation Office (ATO) has issued new guidelines to help you in making a claim for running expenses using the fixed cost method, while working from home from 1 July 2024.

Under this guidance, the ATO will allow you to make a claim of 70 cents per hour for time spent working from home. This claim is a simplified method which includes expenses for:

Energy expenses (electricity and/or gas) for lighting, heating/cooling and electronic items used while working from home

Internet expenses

Mobile and/or home telephone expenses, and

Stationery and computer consumables. This means you cannot claim an additional separate deduction for any of these expenses. For eg, if you use your mobile phone when you are working from home and when you are working from somewhere other than your home, your total deduction for the income year will be covered by the hourly fixed rate.

However, under the revised fixed-rate method, a separate claim can be made for depreciation and repairs and maintenance on furniture and equipment.

In order to make this claim, you will need to keep:

Evidence of additional expenses incurred in the form of monthly/quarterly bills or purchase receipts

A diary of the days you work from home, this can be backed up by evidence such as your timesheet or a roster, and Contact us

With tax time approaching soon, if you require any more information about calculating this deduction, please let us know and we will be happy to assist you further.