A business credit card could be an excellent way to start building your company’s credit profile. We’ve listed five benefits of applying for a business credit card.

At the early stages of your start-up journey, access to credit can be a lifesaver.

Cashflow is tight, customer revenue can fluctuate wildly and large-scale bank loans and external funding may be in short supply. In this situation it might seem counterproductive to apply for a business credit card – a move that adds to your debt level.

But, in fact, applying for a company credit card and using that credit facility responsibly can have a hugely positive effect on your ability to fund your growth and access lines of credit. Let’s explore five ways that a business credit card can improve your funding

Builds up your business credit profile

When you use a business credit card responsibly, and pay off the repayments each month, this starts to build up a credit history for the company. This credit profile is directly linked to your business and is separate from your own personal credit.

Having this credit history (and the associated business credit score) is crucial when applying for business loans and accessing future, large credit lines.

Establishes you as a responsible borrower

Paying your credit card bill on time each month demonstrates your financial discipline and an ability to manage debt in a responsible way.

When applying for loans, bank overdrafts and trade credit, lenders want to know that you’re a low-risk business to lend to. Responsible payment behaviour acts as an indicator of trustworthiness for future borrowing and will increase your chances of successful funding.

Provides a flexible line of credit

Having a business credit card makes it easier to cover your expenses and overheads.

A credit card gives you flexible, accessible funds for your day-to-day operational needs. It’s also an excellent way to cover any unexpected expenses or cashflow gaps. Managing this line of credit also prepares you for larger, more formal, credit facilities.

By not maxing out the available credit on your credit card, and keeping utilisation low, you can show that your business manages debt in a sensible way. This marks you out as a low-risk borrower – a key factor in accessing further credit, business finance and investment..

Acts as a gateway to more favourable terms

By being responsible with your credit use, you set the foundations for a business credit profile.

A solid track record with a business credit card may lead to pre-approved offers for larger credit lines, better interest rates and more flexible terms from banks. This is incredibly helpful as you scale the business and need additional funding to drive your growth journey. Talk to us about applying for credit and business finance

If your startup is in need of an increased cash runway and improved access to credit, applying for a business credit card is an excellent way to improve your financial flexibility.

Come and talk to the team about ways to embrace this kind of credit.

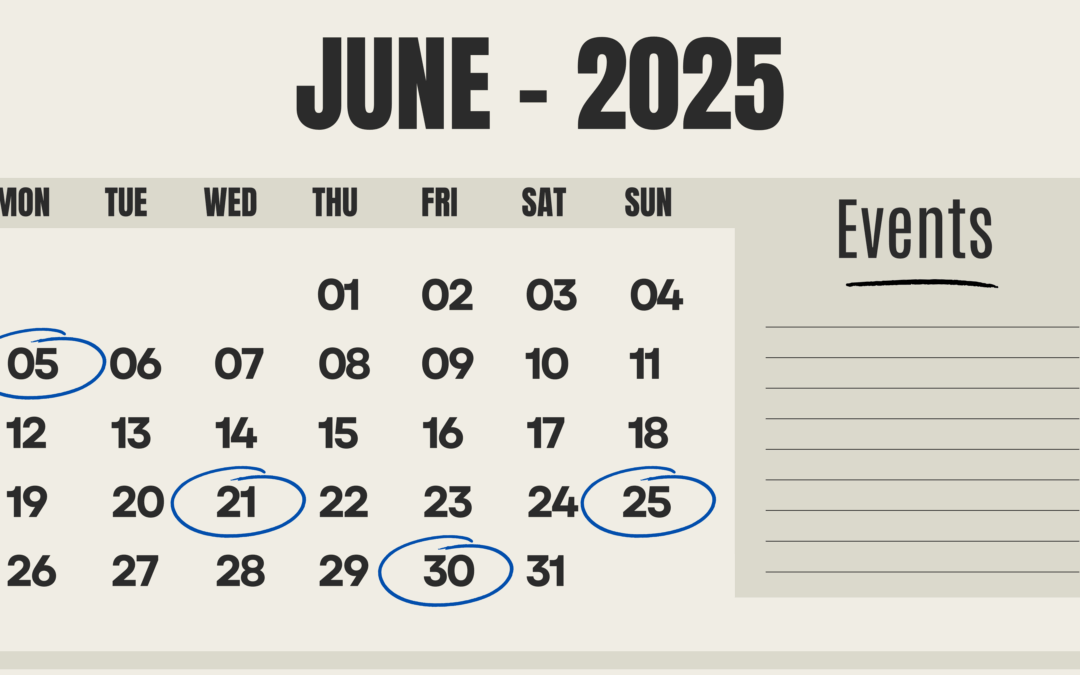

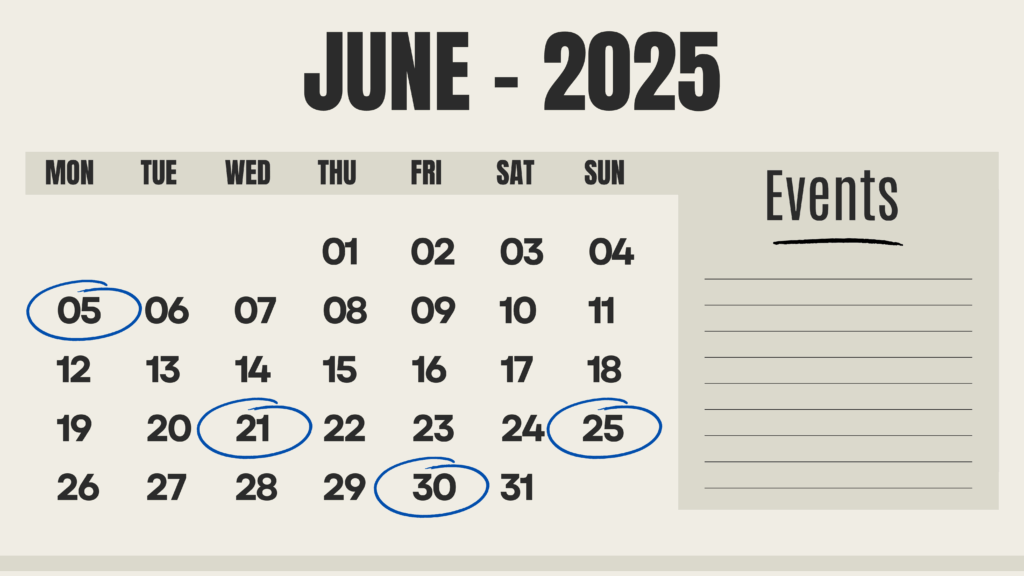

With the end of the current tax year upon us, please do not forget about your final tax obligations for 2025. Here is a list of key tax dates for June 2025.

The end of the current financial year is upon us. For most of you, this means preparation to start finalising your general ledger accounts for the upcoming end of year compliance.

In order for you to be across all upcoming due dates and deadlines, please find a list of the key compliance dates below for June 2025. Make sure these lodgments are up to date to avoid any interest or penalties.

KEY TAX DATES – JUNE 2025

5 June 2025 – Income tax – Due date for lodgment of tax returns of all entities 5 June concession. Note: Entities eligible for the 5 June 2025 concessional due date can lodge by 8 June 2025, as long as any liability due is paid by this date. You do not need to apply for a deferral.

21 June 2025 – GST – Monthly Activity Statement and payment for May 2025

21 June 2025 – PAYG withheld and PAYG instalment – Monthly Activity Statement and payment for May 2025

25 June 2025 – FBT – Lodge 2025 FBT annual return for tax agents if lodging electronically, if you are lodging with us

30 June 2025 – Superannuation guarantee – Super guarantee contributions must be paid by this date to qualify for a tax deduction in the 2024–25 financial year.

We’re here to help if you’re facing operational issues, tackling people challenges, or have health and safety questions, give us a call, email or text us.

The way to calculate a working from home deduction using fixed cost method for additional running expenses has been adjusted from 1 July 2024, with the ATO issuing a new hourly fixed rate.

The Australian Taxation Office (ATO) has issued new guidelines to help you in making a claim for running expenses using the fixed cost method, while working from home from 1 July 2024.

Under this guidance, the ATO will allow you to make a claim of 70 cents per hour for time spent working from home. This claim is a simplified method which includes expenses for:

Energy expenses (electricity and/or gas) for lighting, heating/cooling and electronic items used while working from home

Internet expenses

Mobile and/or home telephone expenses, and

Stationery and computer consumables. This means you cannot claim an additional separate deduction for any of these expenses. For eg, if you use your mobile phone when you are working from home and when you are working from somewhere other than your home, your total deduction for the income year will be covered by the hourly fixed rate.

However, under the revised fixed-rate method, a separate claim can be made for depreciation and repairs and maintenance on furniture and equipment.

In order to make this claim, you will need to keep:

Evidence of additional expenses incurred in the form of monthly/quarterly bills or purchase receipts

A diary of the days you work from home, this can be backed up by evidence such as your timesheet or a roster, and Contact us

With tax time approaching soon, if you require any more information about calculating this deduction, please let us know and we will be happy to assist you further.

To maintain a healthy cash flow, you need more than just strong revenue. Improve your small business cash flow by implementing Five Simple Cashflow Rules.

Need a hand managing cash flow? You’re not alone. The key is getting your invoicing right, by invoicing customers as soon as possible and using tools like Xero’s invoice reminders to move payments along.

That said, there are a few other simple rules you can apply to manage your cash flow and get your invoices paid even faster:

Keep your books accurate and up to date – so you can see your financial state at a glance.

Don’t be too lenient with your customers – you can be direct and still polite. Keep a close watch on your accounts receivable turnover at all times and act sooner rather than later.

Keep your accounting simple – so you have a good handle on these business metrics. We can help with this.

Keep your business and your professional finances separate – this is essential to understanding your true cash flow position. Mixing your business and personal finances can leave you uncertain about business performance.

Build a cash reserve – so you are prepared for unexpected events and can take advantage of opportunities when they pop up.

First you want to get your invoicing right. Get into a habit of sending invoices quickly. Then follow the steps above to collect revenue and keep your finances organised.

Get in touch for guidance on your invoicing and business cash flow.

The sun is shining, the end is near, and we begin to look forward to celebrating with friends, family and coworkers. As your advisor we wanted to make sure that you are fully aware that the end of year celebrations that you put on for your employees may hit you with unintended tax consequences. This message is to provide you with information so that you are fully informed.

Christmas Parties

These are some common scenarios relating to work Christmas parties, and their tax consequences:

Party held on business premises

Where the party is for current employees only, there is no fringe benefits tax (FBT) to pay. However, there is also no income tax deduction or GST credits claimable.

If the party includes current employees and their associates or some of your clients, it depends on how much the cost of the party is per head.

If your party costs less than $300 per head, then there is no FBT to pay, but also no income taxdeduction or GST credits claimable.

If the party costs more than $300 per head, then the amount that is attributable to your employee’s associates (such as their spouse/partner) is subject to FBT. Any amount that is subject to FBT is claimable as a tax deduction, and you can claim GST credits as well. All the other amounts are not subject to FBT, but also are not deductible for income tax and no GST credits to claim.

Party held away from business premises

If the party costs less than $300 per head, then no FBT is payable. However, you also cannot claim a tax deduction and no GST credits are available to claim.

If the party costs more than $300 per head, then FBT is payable with respect to each employee that attends, as well as their spouse/partner. Again, if FBT is payable on an amount, then you can claim an income tax deduction as well as any GST credits.

If any clients of yours attend the party, and it costs more than $300 per head, then no FBT is payable, but also no income tax deduction or GST credits can be claimed.

However, if the party costs less than $300 per head, and at the party guests are provided a hamper (or other non-entertainment gift) worth less than $300, then the hamper is allowable as a tax deduction and GST credits can be claimed.

This is because the hamper is considered a gift which is separate from the party.

Christmas Gifts

If you provide your employees with a non-entertainment Christmas gift to thank them for their service, there is no FBT payable as long as that gift is valued at less than $300. Examples of non-entertainment gifts include a Christmas hamper, a bottle of wine or spirits, giftvouchers, flowers or other similar types of gifts.

If your are not sure where you stand with your holiday gifts and entertainment get in touch and we can help.

More than ever, cashflow is a vital part of staying afloat, whether your business is in recovery or growth mode. Revenue, profit and your bottom line all deserve your attention. But keeping everything running is the baseline.

Regular cashflow forecasts help you keep that in focus. Here’s why:

Cost control – If you can’t reach your targets for income, reining in your costs may give you a little extra head room to manage cashflow while you plan your next move.

Visibility on outgoings – Cost control can be a challenge when it’s hard to pinpoint hidden costs or where established ways of doing things cost more money than they should. You may also have been coping with unexpected expenses, as you’ve adapted your business for unplanned circumstances or increased costs.

Improving business practice – It’s more than only keeping an eye on outgoings (though that’s important). It’s about looking at each aspect of your business and business systems (or the gaps where there should be business systems) to see if poor practice is driving costs up unnecessarily.

It can be useful to break it down – You can look at cost centres such as office supplies or freight. Or you can look at what those costs do for your business. It can help to analyse costs in terms of cost of sale and overheads.

Cost of sale and overheads

Cost of sale (also known as Cost of Goods Sold or CoGS) is how much it costs you to make a sale.

In a business that sells products, CoGS is based on the price paid for the product, plus any costs necessary to put the merchandise into inventory and make it ready for sale, including shipping and handling. You can even break it down to calculate the cost of sale of individual units.

Overheads are general business expenses. They can’t be tracked directly to sales. Overheads are what it costs you to open your doors (whether online or actual) every morning.

What’s your plan?

Reduce unnecessary expenses – Trim expenses that aren’t related to your core product or service.

Suppliers – Are you able to work with your providers to ask for discounts or more favourable payment terms on either cost of sale or overhead expenses?

Talk to your team – Analyse your costs and involve your team, including frontline sales staff.

Efficiencies – Are there efficiencies that could save you money, this can be anything from reducing shipments from suppliers or between stores, to taking advantage of AI to save you time, money or both.

Advertising – It might be a false economy to cut back on advertising, as customers are always looking for bargains and price-checking alternatives. But would targeted campaigns work better?

Prioritise – Can you pinpoint products most likely to bring the fastest or best return and hold back on products that are a slower sell?

Promote or discount – If you have old or slow-moving stock, can you discount it and convert old stock to cash? If you attract customers now, you may be able to use it to spotlight other products.

Every dollar you pull back from your costs can go straight into cash flow. Talk to us if you’d like to review your costs and your systems to keep costs under control. Whether your sales are boom or bust, make sure your costs aren’t holding you back.